Intuitively we know that one of the largest single risks facing a defined-benefit pension fund is longevity – that of its members living longer. Techniques exist to quantify this risk, but for several reasons it remains difficult for pension funds to properly “deal” with this risk within their existing framework :

1. It doesn’t feel like a risk when you only observe it every 3 years : while longevity experience (actual vs expected deaths) can be monitored on an ongoing basis, the risk is only really crystallized every 3 years when the scheme actuary sets his or her longevity assumptions underlying the actuarial valuation, which makes it different to financial risks whose downside (or upside) is felt on a much more frequent basis in the valuation of assets and liabiltieis

2. It doesn’t feel like a risk when it always moves in the same direction: recent experience of this risk has been exclusively in one direction – actuaries revising their expectations toward longer life expectancy and better future longevity improvements (the progression of assumptions used was well summarised by my colleague Muqiu Liu here, my colleague Wenyu Bai summarised and quantified the effect that changing longevity assumptions have had on pension schemes here )

3. It doesn’t feel like a financial risk when the market for transactions is so limited: The market for longevity risk is different to a lot of financial markets in that it is illiquid and subject to significant transactions costs, meaning that the concept of marking-to-market does not exist in the same way.

These issues combine to mean that representing longevity risk alongside asset-side risks in terms of a one year tracking error is a bit unsatisfying and probably not the most suitable framework in which to asses the risk. Nevertheless, to be consistent with other risks in the portfolio this approach is often adopted. The question is, what next?

There are essentially two clear actions a scheme can take to address longevity risk :

1. Hedging

2. Reserving

Most of the analyses I have seen conclude that longevity risk when represented as an annualized tracking error on the whole liabilities is of the order of 3-5%p.a. The beauty of diversification then means that when a low (or zero) correlation is assumed with the other financial risks in the portfolio, the conclusion is that the overall effect on the pension scheme’s risk position of removing longevity risk is not substantial. Add to this the fact that the most readily available longevity hedging solutions can only tackle pensioners and older deferred members and the conclusion starts to emerge that focusing on longevity risk doesn’t “move the dial” in terms of a schemes overall risk, this is assuming that a substantial amount of interest rate and financial market risks remain in the pension scheme as illustrated for a sample pension scheme below.

Notes : Scheme investment strategy 45% equity 55% matching assets. 75% funded (gilts flat basis) Liability hedge ratio 40%. Liabilities 75% inflation-linked

The chart shows that while longevity risk by itself might carry a 1-year VaR95 of around 5%, the effect of diversification means that adding this risk in only increases the overall var from 21.0% to 21.6%.

Given that longevity hedging is generally only available on the pensioner population and older deferred members, this means that, most ALM models will give the result that for schemes in the above situation, transacting a longevity swap will not meaningfully impact their overall risk position.

Many pension schemes in this situation then might adopt the approach of reserving, and by this I mean setting their investment strategy to target a level of expected return slightly above that which they need to meet their funding goals.

What is this level ?

It is really hard to say with any certainty what this level should be but our research suggests that every 0.25% increase in the long-term rate of longevity improvements equates to an expected return requirement of circa 0.20% per annum for a scheme looking to fund this over 10 years. Extending the horizon to 20 years reduces the additional return requirement to around 0.1% p.a.

Achieving either of these increased return targets would clearly require changing the investment strategy to incorporate higher return (and hence higher risk) assets, the quantum of change would be non-trivial but achievable (for example moving roughly 10% of a scheme’s total assets from investment grade corporate bonds into equities, or lower quality and less liquid forms of debt would achieve a 0.2% p.a. increase in return).

There are a couple of sources that might help a scheme decide the level it tries to reserve to:

- In KPMG’s Pensions Accounting Survey 2013, they suggest that the most-used assumption in 2013 by UK pension schemes is a long-term rate of improvement of around 1.25%. This suggests that schemes currently not using this assumption might consider reserving to at least this rate.

- Year on year changes in realised improvements are volatile, but have ranged between 1% and 5% over the last decade. clearly reserving for a situation where improvements continue at the upper end of this band is unrealistic (better to hedge, which can be done well below this level).

Beyond this its really hard to find sensible adverse scenarios to put a number on the level which long term longevity improvements will tail off to in the long term. The Actuarial profession published a paper reviewing assumptions across countries, and although the approaches differ substantially (and most countries do not use a model approach that explicitly calibrates the long-term rate of improvement as a parameter) the paper illustrates that there was an implicit assumption adopted regarding longevity improvements since the previous version of this work in 2005, and this varied between 1 and 2.5% p.a.

But if our scheme becomes better funded, or de-risks over time, when does a longevity hedge start to be an attractive way of taking more risk out?

What I have done below is run a very simplified* ALM analysis for a pension scheme over many different funding levels and asset allocations. Longevity is assumed to carry a 1 year 95% VaR of 5% and have zero correlation with other risks in the portfolio. I have illustrated the relative risk reduction (ie, the fraction of the total risk that is removed) by hedging longevity at various funding levels, hedge ratios, and allocations to risky assets.

the conclusions are pretty clear :

1. Unless the scheme’s hedge ratio is maintained at or close to the funding level, removing longevity is unlikley to remove a large part of the overall risk- better concentrate on hedging interest rate and inflation risks first.

2. As the scheme’s funding level (and hedge ratio) increases, and the allocation to risky assets decreases then the impact of a longevity hedge becomes much more significant. this is intuitively obvious, but we can put some approximate numbers around it :

The really significant reductions in risk come at funding levels (on a gilts flat basis) of 80% or more, and risky asset allocations of 20% or less. here a longevity hedge can remove a quarter or more of the total risk facing the scheme.

On the contrary, if the allocation to risky assets is 40% or more, then a longevity hedge is unlikely to remove more than 10% of a scheme’s overall risk – not an insignificant proportion but probably not a primary focus.

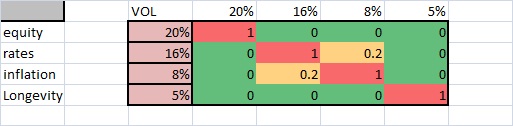

* Simplified analysis models the risks faced by a pension scheme as only interest rates, inflation, longevity and equity (or “risky asset”) with the following covariance matrix:

Scholarly article : Liu, Bai, Mikulskis : Unpredictable Life, Predictable Expectancy? The Impact of Future Longevity Improvements on Pension Fund Investment Strategy – Institutional Investor Journals Fall 2013 p73-78

Available at: http://www.iijournals.com/doi/abs/10.3905/sp.2013.2013.1.073#sthash%2Eo6KyK93n%2EzX1qaMVo%2Edpbs – See more at: http://blog.redington.co.uk/Articles/Muqiu-Liu/October-2013/THE-CHALLENGE-OF-LONGEVITY-FORECASTING.aspx#sthash.Bx86xyTg.dpuf