Q. If I invest an amount of money in equities, what is the cost of protecting this amount over 20 or 30 years ?

We can answer this relatively simply, invoking the Black-Scholes equation. We can set the risk free rate to around 3% (approximately the 20-year swap rate) and the equity dividend yield to around 2.5%. What we are interested in are European vanilla put options struck at 100% with a maturity of 20 and 30 years. The only remaining parameter we need to decide on is the implied volatility. For such long time periods this is not easily observable in the market, but a value of 20% seems pretty reasonable as this is around the implied volatility of the longest dated options that do exist, and also around the long term realised volatilityof markets such as the FTSE 100 and S&P 500.

Putting all these parameters into the pricing equation gives a premium for this put option of around 18% of the original investment amount – really ??

This does seem surprisingly high, given a natural expectation that over a 20 or 30 year period equities will increase in value substantially and the amount of the initial investment might be expected to only be 40% or less of the final amount.

However, it gets worse, what if there is an annual management fee on this equity portfolio of around 1% p.a. (not uncommon in retail or even DC pension arrangements), and we want the guarantee still to be in place at 100% of contributions, even net of the management fee. This is equivalent to raising the strike price to 120%-130% of the original level, and results in an option premium of over 20% of the original sum.

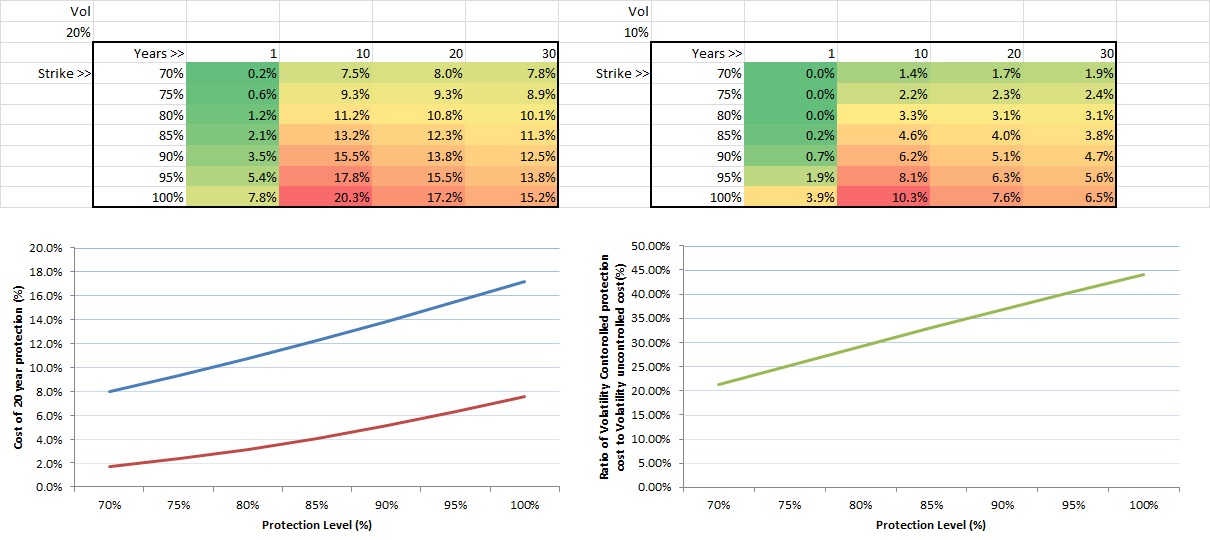

Q. What factors is this premium sensitive to ?

In a mathematical sense, the premium of options is quite transparently related to a number of underlying variables, the most important among these are the time until expiry of the option, the protection level (or strike price) of the option and finally, the riskiness (or volatility of the underlying asset).

Although mathematically the relationship between the premium of an option and the protection level is a little complicated, in a simple sense it looks roughly linear, as shown in the chart below. For a long-term equity option that might have an implied volatility of around 20%, the premium required to protect against the full amount of initial investment (100% strike price) is roughly 18%, if we lower the protection level to 70% of the initial amount invested this decreases to around 8%.

Now you might think there isn’t much we can do to change the riskiness of the underlying asset, given we are investing in equities, but what we can do is employ a volatility controlled approach to investment in equities, where we dynamically vary the exposure according to the ex-post measured volatility of the equity market. By doing this, we can quite successfully control the risk we experience in the portfolio, and this gives us another way of reducing the option premium. What’s more, the proportional reduction in premium is actually greater at lower protection levels.

At a strike price of 100%, the cost of a put option on the volatility controlled portfolio is just under half that of the put option on the volatility-uncontrolled equity allocation. However at lower protection levels such as 70% of the original amount, the cost of the option to protect against falls in the value of the volatility-controlled portfolio is around 20% of the same option on the volatility-uncontrolled portfolio.

Now, there’s a very good reason why the options on a volatility-controlled portfolio are cheaper – they are less likely to be exercised. However, in a Defined-Contribution pension context they could still be useful. In July 2012 Steve Webb, the pensions minister challenged the industry to look at “money safe” investment products that could guarantee to return at least the value of an individual’s contributions. Given contributions into a DC pension are tax-free, then for a basic rate tax payer, for every £78 equivalent of net-tax income, £100 is contributed to the fund. So if we want to look at protecting an individual’s contributions on a net-tax basis, and we employ a volatility controlled approach to investing, then the cost of this contribution is around 2.8% of each contribution made – much more feasible and manageable than the 18% quoted earlier.