Well well well.

I’m sat here on a Sunday afternoon at the end of quite a week. Heading into the office Monday morning I had little idea that we would potentially be caught up in a serious market event that had global ramifications, and at the heart of it all would be the risk management system that’s served clients very well for more than a decade: LDI.

I’ve been generally trying to bring some measured, commonsense explanations to the story. I’ll save more thoughts for Thursday’s newsletter, but for now for folks catching up I’d recommend Toby Nangle’s two blogs for the FT which get a lot of the detail spot on (here and here), as well as Stephanie Baxter’s piece for PP which gives a good, balanced set of views from around the industry.

I think there are still missing pieces here, questions not being asked and other important bits that need to be filled in.

But right now I want to set out as clearly and comprehensively as I can the full context and history of DB pension funds, and their use of LDI, It’s a story in two parts:

- The History of LDI 1997-2021

WHY pension funds did it, HOW it started, key players, key events on the timeline … How we got to now

2. What do higher interest rates mean for DB Pension funds?

Funding levels, asset returns, implications and actions.

Part 1: History of LDI

Here we go. My version my story, recollections may vary.

First, mythbusting: It’s commonly said that regulators forced pensions to do it. 🛑

I don’t fully agree with that. The picture is, at the very least more nuanced than that . Story begins in the late ‘90’s, couple pieces of accounting regs on the way, FRS17 and IAS19. Now companies had to put pension deficits on balance sheets. Suddenly, CFOs and management cared a LOT about pension deficits.

And, for many companies they were massive , hugely volatile & at the whims of interest rates .📈📉

✈️ “Hedge fund with a small airline attached” was the meme of the time for one UK company with a v large pension. In the UK, various legislation around pension scheme liabilities thru the 90’s removed a lot of the discretion on pension payments, making them more like obligations, with contractually defined increase levels

This set the scene for …

💥In 1997 three actuaries produced a key paper: The Financial Theory of Defined Benefit Pension Schemes .

At the time it was hugely controversial. But 10 years later it was becoming conventional wisdom

https://www.actuaries.org.uk/system/files/documents/pdf/financialtheorydefined.pdf

♻️ Effectively it set DB pensions in a financial economic framework for the first time , showing that liabilities could be viewed like a financial instrument – bonds – for risk mgmt purposes like an annuity book and could, should be hedged / matched / defeased accordingly.

AND – market based rates should be used for discounting. Anything else would create discontinuity with reality at some point .

For a time this was v controversial – epic intellectual battles ensued within consulting firms between traditional actuaries and this new paradigm.

For a sense of the philosophical parameters of this debate check out this piece by Anthony Hilton , and my putback. These were years later, but the outlines of the arguments haven’t changed a great deal.

A core corporate finance argument was: shareholders ought to want mgmt take risk in core biz, not in financial markets thru pension (s/holders can get that elsewhere)

🔬In 2001, Boots scheme moved 100% into matching bonds (article here)

Over the following years a few things happened.

📉Plunging equity markets in the wake of dot-com and soaring life expectancy led to many schemes closing to new members. This was important, as they now conformed more clearly to the archetypes in the theory. The investment target for DB schemes fundamentally changed from an open-ended growth objective to an objective more clearly defined relative to a specific set of liabilities.

The idea of the “economic value” of the liabilities (discounted using a market rate like swaps rather than expected asset returns) became the dominant paradigm .

🔁

The first swap based LDI was done in 2003 with the friends provident pension scheme (link below to story)

A decade of Liability Driven InvestingTen years ago, Paul Cooper, Philip Moore, Graham Aslet and the Friends Provident trustees dared to be different. Why? They all understood the challenges of balancing investment risk and return to meet…https://robertjgardner.co.uk/2013/12/21/a-decade-of-liability-driven-investing/

The pitch at this stage, usually by bankers to company management NOT trustees was:

See those wild swings on your balance sheet from pensions? 🎢

Well, they could get a LOT worse 😳

Could even be bigger than your market cap 😖

But we can fix it for you ✅

The Pensions Act 2004 set a lot of the foundations for next 20 years of DB pensions, it established the pensions regulator, the pension protection fund (PPF) , and a system that focused on funding level (assets divided by present value of liabilities).

I come into the picture 2003 👋, fresh investment grad at Mercer. first transactions I worked on were circa 2005. Often financial companies early here – made sense they would see liabilities thru financial lens. Lot of work building models to support advice. Actuary stuff 🤓

LDI held up well in the ‘08 crisis. There were pension funds who had swaps with Lehman, turned out fine. A few changes to credit assessments , but things carried on. By now power shifting from banks to asset managers and consultants. Banks no longer main protagonists as LDI went mainstream. They became commodity providers of derivatives into the asset management programs run by managers. Investment consultants, trustees key driving force.

Pooled funds started getting launched in the late 00’s and early 10’s. This Institute of Actuaries Working paper provides a useful contemporary report from 2007.

By 2013 , industry surveys were showing c£500 bn of liabilities hedged , and 3 managers came to dominate …

One change post crisis was with gilt curve perennially above swaps, the basis of these programs shifted from swaps to gilt repo. The 2068 index linked gilt was issued in 2013 , then a 55 year linker . That helped structuring these programs on gilts

During QE and the big yield falls of 2014-18 LDI helped stabilise funding levels , reduce deficits and contributions. During this time it became pretty much standard house view from main consulting firms, who are v influential in trustee decision making in Uk

This was also the nadir of scheme funding (source: PPF)

That’s why derivatives & leverage became important, schemes needed to invest in growth assets too , as well as hedge liabilities, so just plonking all your assets into gilts to do matching was not great, as that left the company on the hook to fill a big deficit. Schemes needed to match liabs AND earn gilts +2-3% on assets

You can see why the bit of both worlds was a big attraction

As yields fell, value of LDI portfolio swelled. Pooled funds paid out distributions to their clients in order to maintain leverage and not let it drift down.

By 2019 it had grown to £1trn , with over a thousand pension funds using it.

Coincided with surge in size of gilts outstanding in decade post-08 (source: ONS)

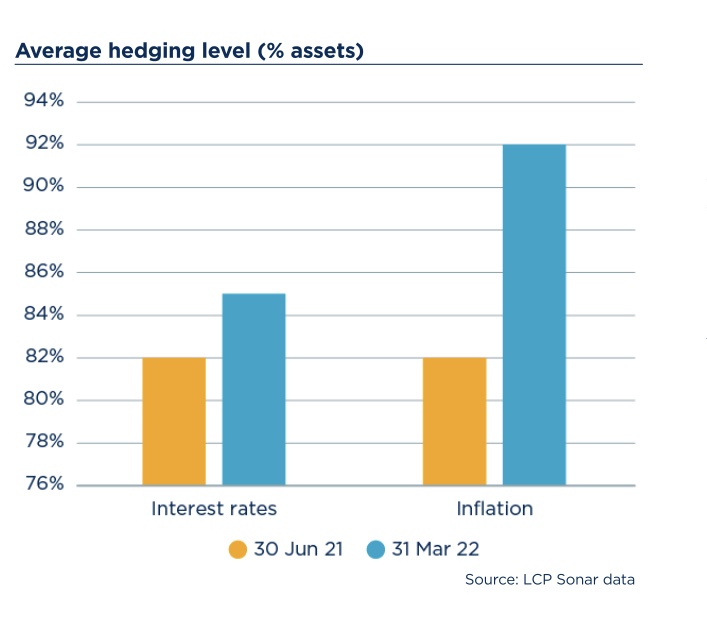

By the start of 2022 , the UK DB segment was £1.8trn (PPF again)

72% was held in bonds, of which 70% gilts ~ £900m (source: PPf Purple book)

About 85% of liabilities were hedged (source: LCP)

Assets sensitivity was c1% (£18bn) for every 0.1% move higher in rates

Brings us almost up to date, quick summary:

- Accounting rules made folks care about volatile deficits

- Financial theory laid down in late 90’s, later adopted by most advisers

- As schemes closed liabs became more fixed, nature of investmet objective shifted

- First hedges done early 2000’s

- Industry grew from there

Part 2: DB Pensions and rising interest rates

What do soaring gilt yields mean for DB pension funds?

There are implications for markets, strategies & managers

Important context: higher gilt yields are generally GOOD for DB pension schemes. Future liabs are discounted at higher rates, so other things equal you need less assets today to meet same liabilities

Eg, I’ve seen some schemes where £ present value of liabilities has ~halved since 2021. They need literally half the assets now to be considered fully funded vs a year ago

But (1) as you probably know most schemes hedge this sensitivity to interest rates. That means they do stuff with their assets, usually involving derivatives to offset the impact of changes in gilt rates

But (2) there are many different measures of liabilities that a scheme will look at and most schemes hedge a portion of one of the lower measures. Might be 60%, might be 70% might be 100%

But (3) those hedges – many via derivatives – will have suffered big mark to market losses and will need more collateral to be placed to maintain exposures (which schemes will generally want to do if possible)

Back to that in a second but to complete the picture on context:

The largest of the possible liability measures a scheme tracks is the BUYOUT liability. That’s the amount you’d need to pay an insurance company to take on the liabilities …

… and that’s the goal of most schemes , to offload assets and liabilities to an insurance co .

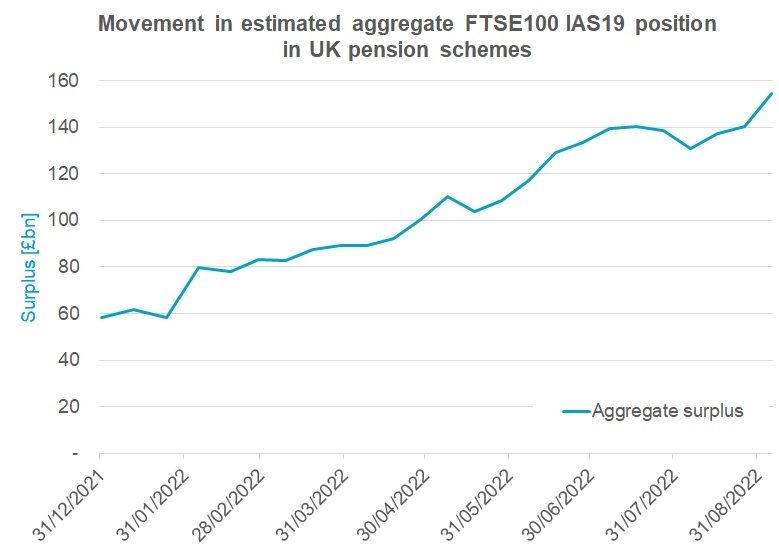

Scheme funding has tracked higher in recent years, but in most cases there’s still been a deficit on this , higher , buyout measure. Not any more. Soaring yields this year have collapsed the gap to buyout that most schemes are seeing In many cases this brings forward their plans by a decade. Eg, planning to buyout early 2030’s (thru investment growth)… but now we’re there already

The result: total mindset shift across the industry from investing for growth to getting in queue for a buyout

A colleague tracks funding of FTSE schemes

So what? Impact: divesting from growthy asset classes and buy bonds (gilts & corporates)

Jonathan Griffith on LinkedIn: #accounting #pensionschemes #ftse100FTSE100 companies now have £150bn+ of surplus in their UK pension schemes on an IAS19 accounting basis. Whilst clearly good news that the position is so…https://www.linkedin.com/posts/jonathandgriffith_accounting-pensionschemes-ftse100-activity-6973242424022163457-HdfW?utm_source=share&utm_medium=member_ios

So, what are pension schemes doing in this moment:

(1) buying / selling gilts

(2) buying / selling other stuff

And what market impacts could it have ?

There will be some DB schemes who were late to get into liability hedging or who never got to 100% hedged. They just had a mega windfall gain vs liabilities and are likely to take the opportunity to get hedging up to 100% > buyers of gilts

Schemes moving into a holding pattern to buyout will also retain gilts as insurers generally hold them too > retain gilts

But what about those mark to market losses in those hedging portfolios ?

Big picture – it’s fine bcos offsets same or larger fall in liabs

But in practice – need to liquidate assets quickly to replace collateral . Typically these hedging programs ran with 100-150bps buffer against rising rates , so already went through one re-collateralisation earlier this year. In many cases will be looking at a second collateral call now , but the speed of this latest leg higher is the problem. Eg some programs have needed to bring forward planned month-end calls in order to keep hedges maintained

Again, big picture not a problem here, as selling assets was always the plan , it’s just happening quicker than thought but places serious operational strain on arrangements. Simply can’t always move funds between diff managers that quickly . In some cases requires signatures and wet ink to move money.

So could def see some accounts reaching levels where they knock-out of their positions and de-lever, this isn’t great and schemes will try and avoid (worst scenario is you knock out of exposure then yields fall when you have no hedge, could easily happen in volatile world). Any such knocking out of positions would contribute to forcing yields higher, of course

What about other assets , what are schemes selling ?

Mainly it’s NOT UK equities these days, majority is global equity and global corporate bonds – no real problems here. Yes might be selling with assets off highs , but GBP helps w some of that. And anyway, you don’t get to sell every asset at highs, it’s just not realistic

Question marks in private markets / illiquid assets

One example there is UK property. It’s not a big allocation for schemes, but UK DB schemes are quite big holders of the asset class, and quite a large number of them are likely looking to get out. Possible we see gating of funds there. Another example is infrastructure funds . Could be open ended with periodic liquidity. Ownership there likely to be more dispersed though and many funds actually have queues to get in anyway

So, if you’ve followed this far 😅

A summary –

Higher yields generally good for DB schemes

Some will want to buy more gilts

Other stick with holding but face losses& operational issues meeting collateral

Will look to sell what they can to meet collateral

One thought on “LDI: how we got to now”